dossierpret

Analyze your mortgage file before the bank does

DossierPrêt Wants to Be the Friend Who Reads the Fine Print Before You Sign Anything

The Macro: The Bank Already Has Software. Now You Might Too.

Here’s the thing about mortgage applications that nobody really talks about: the bank runs your file through a scoring model before a human ever looks at it. They have tools. You have a folder of PDFs and a vague sense of dread.

That information asymmetry is old, but it’s only recently that anyone’s seriously tried to close it from the applicant side. The pitch used to be financial advisors and mortgage brokers, people you pay to translate bank-speak. That works, sort of, if you can afford it and if you happen to find a good one.

What’s changed is that structured financial data is more accessible than it used to be, and ML-based scoring logic (the stuff banks actually use) is documented well enough that you can build something approximating it on the consumer side. That’s a real shift. A few fintech players have been circling this problem from different angles. Some focus on credit score optimization. Some build broker-facing tools. Some are straight-up mortgage marketplace plays that want to own the transaction. What’s less common is a product that sits squarely in the “help the borrower understand their own file” lane, before any application gets submitted.

The productivity software angles here are real but secondary. The more interesting frame is: who owns the diagnostic layer in consumer finance? Right now the answer is mostly the lender. Products like Cushion, which has been rethinking how people manage financial stress through their existing tools, suggest there’s appetite for software that sits on the borrower’s side of the table. DossierPrêt is betting the same thing, specifically for the mortgage moment.

That moment matters a lot. A rejected mortgage application can hurt your credit. Most people don’t know exactly why they got rejected. That’s a real problem worth solving.

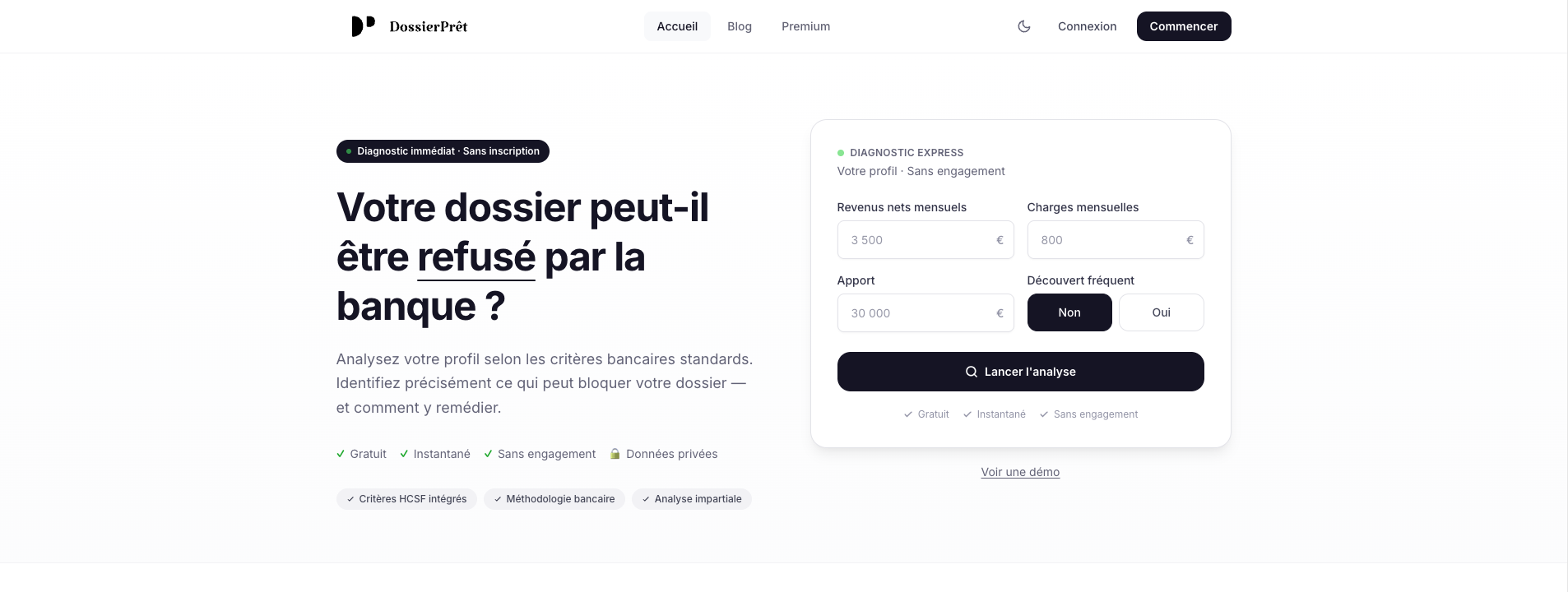

The Micro: A Pre-Flight Check for Your Loan Application

DossierPrêt’s tagline is “analyze your mortgage file before the bank does” and the product is pretty literally that. You feed it your financial information, and it runs a diagnostic, surfacing rejection risks and giving you an approval probability before you submit anything to a lender.

The core use case is obvious once you hear it. You’re six weeks out from wanting to buy a place. You think you’re probably fine but you’re not sure. Instead of finding out the hard way, you upload your documents and the tool tells you what looks weak, what looks strong, and what you might be able to fix before the real submission.

I don’t have access to the product directly (the website wasn’t scrapeable), so I’m working from the product description and the framing, which is French-language or at minimum French-market-oriented given the name. That’s an interesting choice. The French mortgage market has specific documentation requirements (the “dossier” framing is very much a French banking convention), so if this is built around a specific regulatory and documentation context rather than trying to be generic, that’s actually a smarter starting point than trying to boil the ocean across multiple markets.

The three pillars they list, detecting rejection risks, improving approval chances, and providing a financial diagnostic, sound like three outputs from one underlying model. Whether that model is sophisticated or relatively rules-based, I genuinely can’t tell without getting into the product. That’s the most important unknown.

It got solid traction on launch day relative to its apparent stage, which tells me the problem resonates even if the product is early.

The closest analogues I can think of are credit monitoring tools that added “score improvement tips,” but those are backward-looking. This is trying to be forward-looking specifically for the mortgage event. That’s a tighter, more useful frame. Like the difference between a fitness tracker and a coach who tells you what to do before a race.

I’d also want to know if it connects to AI tools that can actually act on financial data rather than just surface it, because right now this sounds like a read-only diagnostic. That’s fine for v1. But the product gets more powerful if it can suggest specific remediation steps with real specificity.

The Verdict

I think the problem is real and the timing is reasonable. Anyone who has gone through a mortgage application in the last few years knows it feels like submitting homework and waiting to find out if you passed, with no visibility into the grading rubric. A tool that gives you that rubric ahead of time has genuine value.

What I don’t know: how good the model actually is. A diagnostic tool that gives you false confidence is worse than no tool at all. If DossierPrêt tells you your file looks fine and then the bank says no, you’ve lost trust and potentially time. The accuracy of the risk scoring is everything here.

At 30 days, I’d want to see real user testimonials from people who used it, applied, and got approved. That’s the proof of concept that matters. At 60 days, I’d want to know if they’re expanding the feature set toward actionable fixes or staying purely diagnostic. At 90 days, the question is whether they’re building toward any lender integrations or staying firmly on the consumer side of the table.

The French market focus, if that’s what it is, might be the smartest thing about this. Nail one market’s documentation logic before going broad. That’s how you build something that actually works instead of something that sounds like it works.

I’m watching this one.